Demystifying Double Materiality

Want to know more about Double Materiality? Interested in understanding how Diginex can help? Read more here!

Sustainability reporting, as well as broader corporate sustainability strategies, should reflect an understanding of the most relevant environmental, social and governance (ESG) issues for a business. For sustainability efforts, including the publishing of ESG reports, to be most effective, they should address the issues that are most significant to the business and its key stakeholders – otherwise known as material ESG issues.

The concept of materiality originated in accounting, where it is often defined as the financial information that is likely to influence an investor’s judgement and should be captured in the preparation of corporate financial statements. Similarly, in the context of ESG reporting, materiality is a measure of the importance of ESG-related topics, issues and information for a business.

ESG materiality at a corporate level is often determined through a Materiality Assessment – which involves internal and external research and analysis to identify the key topics your organization should prioritize, and, in turn, include in your ESG reports.

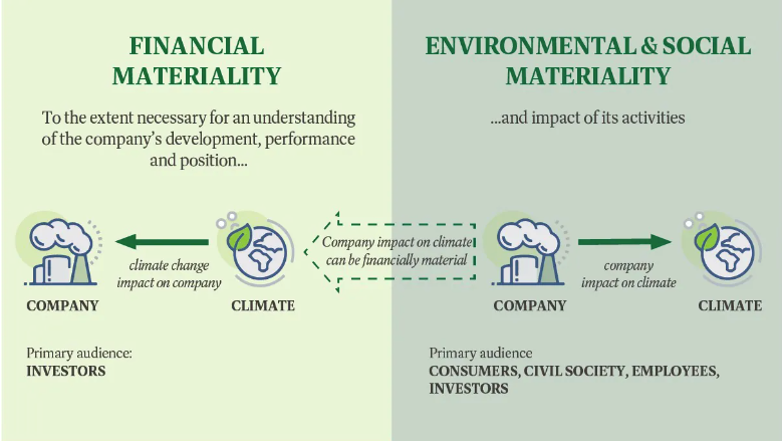

ESG topics and issues can be material from the perspective of how a company impacts society and the environment (outward or “impact materiality”) or vice versa, how the world impacts a company and its ability to operate (inward or “financial materiality”). That is the basis of the concept known as double materiality, first introduced by the EU Commission as part of its regulatory workstream.

For example, a company emitting large amounts of greenhouse gases (GHG) has a negative impact on the environment and people (impact materiality). A government imposing GHG emission regulation may force that company to invest in emission reduction mechanisms, buy offsets or risk paying fines – thereby making the same issue financial material as well. In turn, a company that has operations in areas of high climate risk may identify climate as a financially material issue, even if the company has no significant impacts on climate.

This distinction is important, as ESG reporting frameworks and standards tend to adhere to a specific view of materiality, and key stakeholders may also prefer the application of one or another in corporate ESG reports. The European Union’s Sustainable Finance Disclosure Regulation, adopted in 2019, already requires investors to disclose not only risks to themselves, but also their adverse impacts on both the planet and society. The EU Green Taxonomy and Guidelines on Reporting Climate-Related Information confirm double materiality as the basis for comprehensive non-financial information disclosure. The EU’s Corporate Sustainability Reporting Directive (CSRD), on schedule for implementation in 2023, also incorporates the concept of double materiality.

Want to know more about Double Materiality?

Interested in understanding how we can help? Get in touch with our ESG advisory team here!

Make compliance

your competitive advantage.