CSRD: A New Era of Corporate Sustainability Reporting

CSRD introduces a new era in corporate sustainability reporting, requiring companies to disclose their environmental and social impacts.

Introduction:

The European Union's Corporate Sustainability Reporting Directive (CSRD) marks a pivotal moment in the evolution of sustainability reporting. Aimed at enhancing transparency and accountability, the ESRS introduces a comprehensive framework that extends beyond financial metrics, compelling businesses to disclose their environmental and social impact.

CSRD Basics:

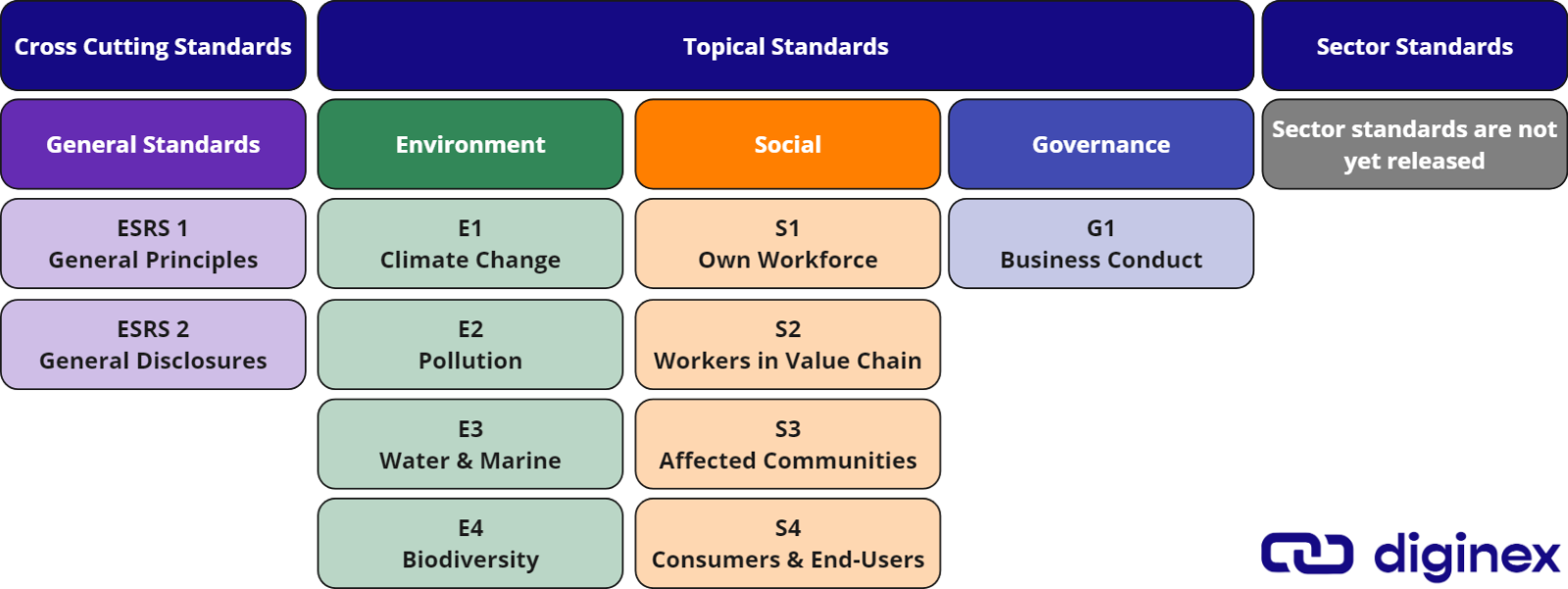

At its core, the ESRS mandates that large companies disclose detailed information on their environmental, social, and governance (ESG) performance. This comprehensive framework covers a wide range of factors, including general disclosures, topic-specific, and sector-specific:

Timelines

The CSRD is being implemented in phases, with different categories of companies facing staggered deadlines:

- Large companies already familiar with NFRD reporting will be the first to adopt CSRD, with their inaugural reports due in 2025 covering data from 2024.

- Large companies not previously subject to NFRD will join the CSRD journey in 2025, publishing their first compliant reports in 2026 cover data from 2025.

- Listed SMEs will also play a vital role in the transition to CSRD, with reporting requirements beginning in 2027 (covering 2026 data) and a potential opt-out until 2028 available for eligible companies.

Double Materiality

The directive also introduces the concept of "double materiality," requiring companies to report not only on the financial risks of climate change (aligning with the financial materiality approach of frameworks like ISSB and SASB) but also on their broader impact on the environment and society, echoing the impact materiality approach pioneered by GRI. This comprehensive, dual lens aims to provide stakeholders with a holistic view of a company's sustainability performance.

CSRD Implications:

The implications of CSRD are far-reaching:

- Increased transparency: Companies must provide more comprehensive and standardized sustainability reporting.

- Strategic integration: Sustainability considerations need to be integrated into core business strategies.

- Enhanced risk management: Better identification and mitigation of sustainability-related risks.

- Investor and stakeholder trust: More transparent reporting builds trust and confidence.

- Competitive advantage: Companies that proactively embrace CSRD can gain a competitive edge in the market.

Conclusion:

The CSRD represents a paradigm shift in corporate sustainability reporting, one that demands a proactive and comprehensive approach. By understanding its nuanced requirements and embracing its forward-thinking spirit, businesses can not only navigate this transition but also seize the opportunity to lead the charge towards a more sustainable and equitable future.\

Diginex is proud to be at the forefront of this movement, offering one of the first software solutions to seamlessly integrate CSRD requirements into your existing reporting workflows. Let us empower your business to not just comply with CSRD, but to truly excel in the era of transparent and accountable sustainability reporting.

Make compliance

your competitive advantage.