ISSB S2 - The New Wave of Climate Regulation?

ISSB's S2 climate standards, informed by TCFD, could be the next global benchmark for climate reporting. Regulators are transitioning from TCFD to ISSB S2.

.svg)

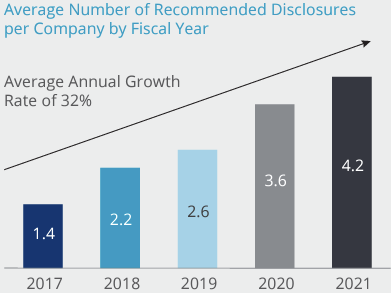

Over the past five years, the world of corporate climate reporting has undergone a remarkable transformation, largely due to the 11 recommendations released by Task Force on Climate-related Financial Disclosures (TCFD) in 2017. With the development of the new S2 climate standards by the International Sustainability Standards Board (ISSB), are we approaching a new era in climate regulation?

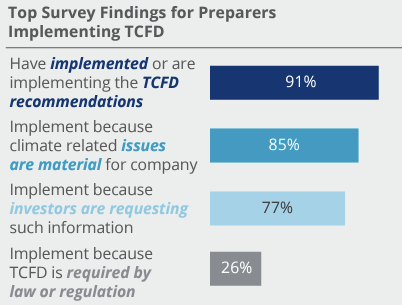

Since its inception under the Financial Stability Board (FSB), the Task Force on Climate-related Financial Disclosures (TCFD) has significantly impacted the prevailing trends and discussions surrounding climate reporting. With 11 recommendations designed to enable organizations to better understand and disclose their exposure to climate-related issues, the guidance developed by the TCFD has been widely adopted by companies, investors, and regulators, driving a global shift towards increased transparency and accountability in climate risk management. The endorsement of influential figures like BlackRock's CEO, Larry Fink, further highlights TCFD's impact as a key driver of climate action.

The ISSB, which was created through the consolidation and support of the worlds leading sustainability reporting initiatives, recognized the value of TCFD's work and incorporated many aspects into it’s developing climate standards. The upcoming S2 standards have been informed by TCFD's framework, underscoring the lasting influence of TCFD has on the latest climate conversations.

However, as the ISSB's S2 standard begins to take shape, regulators are increasingly looking to the ISSB to align their developing climate regulations against the ISSB in lieu of only relying on TCFD requirements, reflecting growing confidence in the ISSB's comprehensive approach to climate-related disclosures. Given the importance of the IFRS Foundation across the globe, the S2 standard could very well become the global benchmark for the next generation of climate reporting.

To further explore this, we can look towards Hong Kong Exchanges and Clearing Limited (HKEX) April announcement as a prime example of how climate regulations are transitioning from TCFD to the ISSB S2. Prior to this announcement, the HKEX had already set ambitious carbon neutrality targets for 2050 and plans to implement mandatory climate-related disclosures aligned with TCFD by 2025. However, with the emergence of the ISSB S2 standards drawing near, the city's regulatory authorities have stated their intent to introduce new climate-related disclosures specifically designed after ISSB’s S2. Their April Consultation Paper provides a comparison of what their current TCFD-related requirements are VS what the latest ISSB inspired requirements could look like.

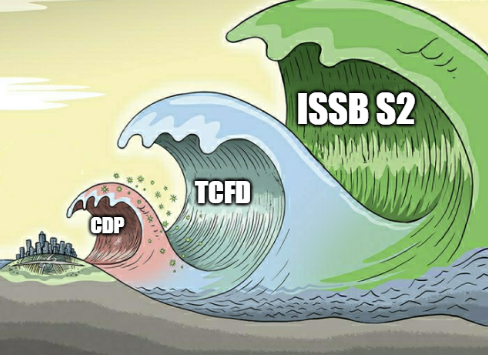

The development of corporate climate reporting has been influenced by many factors over the years, but two of the most paramount have proved to be CDP's climate questionnaire, which was launched back in 2002, and more recently, the publication of TCFD's recommendations in 2017.

Just as TCFD heavily influenced the most popular climate-related reporting questionnaires for corporates (CDP) in years following its release – the ISSB S2 standard may very well drive further advancements in climate-related sustainability reporting on a massive scale.

Looking ahead, ISSB's S2 standard is quickly approaching, and as Hong Kong and even Canada have shown in the last few weeks, the ISSB is already beginning to have an impact on where the next generation of climate-related regulations are headed.

You might think that the ISSB’s S2 standards would naturally follow the introduction of the SASB-inspired S1 standards. Surprisingly, that’s not the case. On April 4th, 2023 the ISSB shared that they're giving priority to the S2 standards for 2024 over S1. This change will undoubtedly draw more attention from regulators and investors to the ISSB S2 standards in the upcoming months. Given the high synergy between ISSB and TCFD, it's a good idea to increase your alignment with TCFD as soon as possible to ensure you're well positioned to ride the next wave of regulatory expectations.

About the Author:

Markus is a specialist in ESG & Sustainability Reporting and at Diginex, uses his passion for sustainability reporting help create the next generation of sustainability reporting software solutions. With sustainability experience gained in academia, industry, and consulting, he has utilized countless sustainability frameworks, standards, and ratings to improve sustainability strategies for companies in a wide variety of industries. Learn more about Markus here.

Make compliance

your competitive advantage.